As we sat around the table eating breakfast this morning we were chewing in quiet contemplation. Seeking to break the silence, I inquired of Mihaela and Noah if they dreamed last night.

Mihaela said, "I did. It was a bad dream. Not Awesome, at all. I don't want to talk about it."

I hate it when my dreams are "not awesome."

Sunday, December 28, 2008

Saturday, December 27, 2008

Just ignore the logic

As we drove to Target we were listening to the Veggie Tales Christmas CD. From the back of the van Mihaela pipes up and says, "Cucumbers can't talk."

I retort: "Larry is a cucumber and he can talk."

To which she replies, "What does that have to with anything?"

Logic is lost on a four year old...

I retort: "Larry is a cucumber and he can talk."

To which she replies, "What does that have to with anything?"

Logic is lost on a four year old...

Monday, December 08, 2008

Weather Advisory Commentary

I absolutely LOVE THIS.

A producer by the name of Ben Bowman (no known relation, although he is smart enough to be related), produces a commentary against his own network's coverage of snow in Chicago. He hits the nail on the head!

A producer by the name of Ben Bowman (no known relation, although he is smart enough to be related), produces a commentary against his own network's coverage of snow in Chicago. He hits the nail on the head!

Tuesday, November 25, 2008

Forsooth!

This guy was DEAD ON. I love how he gets ridiculed, but maintains his convictions. I wonder who is laughing now.

Thursday, October 30, 2008

Fall in New England

I just got back from Connecticut. I went to Hartford to provide training to our web application. I have heard about Fall in New England. I have heard that it is beautiful and there is nothing like it. I figured people were "overselling" and exaggerating. After all, we have the same trees in Alabama. They turn colors. I've lived in Wisconsin. Same kinds of trees and very similar weather. Both Alabama and Wisconsin have pretty trees in the Fall.

Let me tell you. There is a difference. The leaves in New England are brighter. They are more vibrant. There are more shades of the colors. We don't have the golds and yellows and reds and oranges that I saw there.

There was nothing more stunning than flying in over the city and seeing the landscape. Pictures can't capture it. Words can't describe it. You have to go see it for yourself.

Let me tell you. There is a difference. The leaves in New England are brighter. They are more vibrant. There are more shades of the colors. We don't have the golds and yellows and reds and oranges that I saw there.

There was nothing more stunning than flying in over the city and seeing the landscape. Pictures can't capture it. Words can't describe it. You have to go see it for yourself.

Friday, October 10, 2008

Dow takes Nose Dive

Thank goodness Congress approved that bailout. Otherwise, the economy might be tanking.

WHOA!!!! Wait a minute...it is tanking...

SO...the bailout isn't working? How can that possibly be? Our government is on top of this!!! If they can't fix it...then nobody can...after all, no other entity is more dependable and competent than the government, right?

WHOA!!!! Wait a minute...it is tanking...

SO...the bailout isn't working? How can that possibly be? Our government is on top of this!!! If they can't fix it...then nobody can...after all, no other entity is more dependable and competent than the government, right?

Wednesday, October 01, 2008

NYT predicts Sub-Prime Failure in 1999

So many pundits are currently blaming the policies of the failed Bush administration for the current economic crisis.

The internet, however is a wonderful thing. On Sept. 1999 (who was President then?) reported that Fannie Mae was "encourage those banks to extend home mortgages to individuals whose credit is generally not good enough to qualify."

The article goes on to prophesy,

The internet, however is a wonderful thing. On Sept. 1999 (who was President then?) reported that Fannie Mae was "encourage those banks to extend home mortgages to individuals whose credit is generally not good enough to qualify."

The article goes on to prophesy,

"Fannie Mae is taking on significantly more risk, which may not pose any difficulties during flush economic times. But the government-subsidized corporation may run into trouble in an economic downturn, prompting a government rescue similar to that of the savings and loan industry in the 1980's."How can they be so two-faced?

Tuesday, September 30, 2008

Nationalizing Failure

I am not so sure that "financial crisis" is as real or as bad the media and the government wants us to believe. Sure, there is a problem. But, let's just consider the fact that yesterday's Dow dropped 778 points. That sounds just terrible, doesn't it? But wait! When it comes to a PERCENTAGE drop in the Dow yesterday isn't even in the top ten! I don't remember Katie Couric mentioning that fact last night!

I don't know about you, but with every day that passes I'm starting to doubt that this crisis is as dire as they say it is.

The proper answer here is to let private institutions that make bad decisions fail. No government bailout. The only one mitigating factor in favor of intervention might be the Congress' involvement in the Community Reinvestment Act and support for various community groups who used those laws to browbeat private institutions into making bad loans.

The plain fact of the matter is that the Federal Government is in the process of nationalizing failure. Under the ideals being tossed around on Capitol Hill profits would belong to private businesses and losses would belong to the taxpayers.

Advice

The company I work for leases office space in a building. We share some "common-areas" with some other tenants. An older guy who works for one of the other tenants as a "gopher," is a great guy. He is very friendly and personable but I don't think he is quite "all there."

Anyway, when we pass in the hallway and exchange pleasantries, he keeps calling me "Rick." So, do I correct him and tell him my real name? If so, how do I do it without embarrassing him?

Anyway, when we pass in the hallway and exchange pleasantries, he keeps calling me "Rick." So, do I correct him and tell him my real name? If so, how do I do it without embarrassing him?

The "Common Sense" Fix to the Economy

Dave Ramsey has written a three point proposal for getting cash back into the market at a fraction of the cost of the bail-out.

The proposal is one page with bullet points. It makes a lot of sense.

The proposal is one page with bullet points. It makes a lot of sense.

Monday, September 29, 2008

STOCKS PLUMMET!!!!

The media goes into hysteria as the stock market drops after the House votes to NOT bailout the banking industry.

WHAT A SHOCKER!!!

It only makes sense that the stock market would drop. See, the stock market it just an indicator of how confident people are in the economy. The fact that we were talking about a bailout show that there is a problem. Why would people be confident? The only thing keeping it from happening it earlier was the hope that the government would resurrect the banking industry. Although why people would be anymore confident when the government 's finger is in the middle is beyond me.

So, people LOST confidence in the economy a couple of weeks ago. The market didn't show that loss because of a pending government bailout. When the bailout didn't happen, the people were able to act on the confidence they lost weeks ago.

It will be important to note that the stock market didn't crash today because government failed to act. It failed TODAY because the government promised to act weeks ago. The promise of "doing something" only delayed what should have happened...

Let's see how many pundits point that out. (I wouldn't hold my breath if I were you).

WHAT A SHOCKER!!!

It only makes sense that the stock market would drop. See, the stock market it just an indicator of how confident people are in the economy. The fact that we were talking about a bailout show that there is a problem. Why would people be confident? The only thing keeping it from happening it earlier was the hope that the government would resurrect the banking industry. Although why people would be anymore confident when the government 's finger is in the middle is beyond me.

So, people LOST confidence in the economy a couple of weeks ago. The market didn't show that loss because of a pending government bailout. When the bailout didn't happen, the people were able to act on the confidence they lost weeks ago.

It will be important to note that the stock market didn't crash today because government failed to act. It failed TODAY because the government promised to act weeks ago. The promise of "doing something" only delayed what should have happened...

Let's see how many pundits point that out. (I wouldn't hold my breath if I were you).

Saturday, September 27, 2008

Is the Economic Bailout Wise?

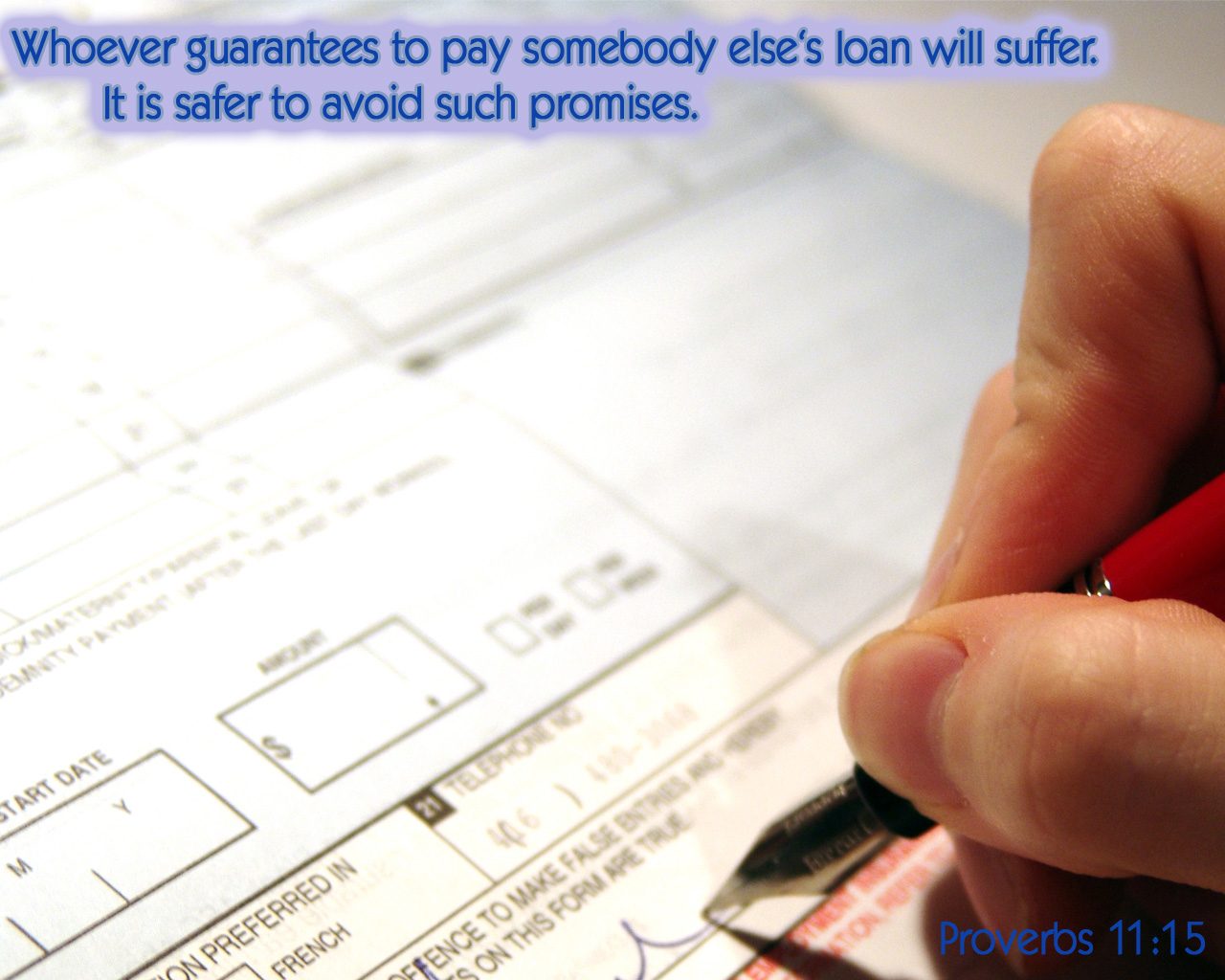

While preparing announcement and scripture slides for church tomorrow, I ran across a scripture slide I made a while back. It made me smile thinking about Congress' current plan to help the economy. My main view is that a bailout is short-sighted; it will fix the problem here today, but will cause many more problems in the future. Man that sounds an awful lot like this scripture:

Proverbs 11:15

Proverbs 11:15

Proverbs 11:15

Proverbs 11:15Friday, September 26, 2008

Everyman's Guide to the Financial Crisis

I've been trying to really wrap my mind around the so-called "Financial Crisis." I am confused because I don't see a crisis. Nobody I know at church, work, or family seem to be affected by the "crisis." Sure, prices on gas and groceries are higher, but most people are just cutting back or making small changes in their lifestyle. So, I'm not sure what the crisis is.

However, even smart, economic people seem to think that there is a crisis. So, even though I don't see it, I need to understand it because my children and I look like we will be paying for "the solution." Here is my very poor attempt to distill the complicated problem into a simple explanation that can be understood by "everyman."

How banks work

To understand the problem, we need to first understand how banks work. Banks make a profit by loaning money. The funny things is that they don't loan their own money, they loan our money. We deposit our money in a bank to keep it safe for us. The bank then turns around and gives it to someone else in order to make money for itself. Banks can legally extend considerably more credit than they have cash. Still, most of us have total trust in the bank's ability to protect our money and give it to us when we ask for it.

Think back to Jimmy Stewart in "It's a Wonderful Life." There is a scene where there is a "run on the bank." A "run on the bank" is a panic that occurs when a large number of customers of a bank withdraw their deposits because they fear the bank is about to fail. So, all of the people who have deposited their money with George Bailey are clamoring for their money back. George tries to explain that he doesn't have their money, that it is tied up in other people's homes. He says,

The Bank's Cash Reserve

So, banks make money by making loans. The amount of money a bank can lend is set by the Federal Reserve. This money that the bank is not allowed to lend is called the reserve (the reserve requirement is currently 3 percent to 10 percent of a bank's total deposits). This reserve is used to pay-out when bank customers need to use their money.

How The Mortgage Loan Industry Works

So, this crisis has its roots in the "sub-prime" mortgage industry. Basically, it used to be that to get a loan from a bank to buy a house it took a 20% down payment, several years at the same job, a great credit score, etc... These are all hard things to get. Saving up 20% of the purchase price takes fiscal discipline over a sustained period of time. It showed banks that you were a responsible and disciplined individual who could be trusted.

As you can well imagine, these requirements were a barrier to home-ownership. It was hard to get in a position to be eligible for a loan. Home-ownership is one of the primary means of building wealth. The government thought it would be good to help people achieve home ownership so that people could build long-term wealth. They, therefore, set up some programs with lower hurdles to jump.

One can now get FHA loans, VA loans, and other loan programs that do not require the same standards of fiscal discipline. I actually have an FHA loan and was able to get a mortgage with a pitiful 3% down-payment. The banks are willing to give people without a proven track record of financial discipline a loan because these types of loans are insured by the Federal government. If I fail to pay my mortgage, then the bank knows that the Federal government will pay-off the loan. The bank will not lose its money so it loans the money to people that are more likely to default on the loan.

In an effort to loan even more money, banks created new type of loan known as "sub prime" loans. These are loans that are made to people that do not meet Fannie Mae or Freddie Mac guidelines. Reasons for this might include credit status of the borrower (they have declared bankruptcy in the past, are consistently late on credit card payments, etc...), income and job history, and income to mortgage payment ratio (FHA guideline don't allow for the mortgage payment to be more than 38% of your income). So, now banks are loaning money to people who are at a much higher risk of defaulting.

Reselling Loans

Now, this where the banks began to be "greedy"1. Most banks and mortgage brokers DO NOT HOLD the loans they make. Once the loan is made is to an individual, the bank will then sell loan to another bank or investment firm. So, say the bank gives you a loan for $250,000 for 30 years at 6.5%. Over the next 30 years you will pay a total of $568,000: $250,000 (principle) and $318,000 in interest (i.e., that is the bank's profit). Well, a bank doesn't want to wait 30 years to get thier profit. So, they will sell the loan to someone else for $350,000. The bank gets an immediate $100,000 in profit and the investment firm is happy with $218,000 in profit (after 30 years).

Of course, the bank doesn't just sell one mortgage to the investment firm. Instead, they will package 100 mortgages that they originated all together and sell those to the investment firm. The investment firm doesn't look at the risk associated with each individual loan the bank originated, but a the package at whole. Some unscrupulous banks and mortgage brokers (knowing they would resell loan and not be liable for the risk) gave loans to people they knew could not repay the loan. These unscrupulous lenders would then misrepresent the risk of the package to the investment firm by mixing the package with both low-risk and high-risk loans.

The Housing Bubble

Easy access to home loans led to lots of people wanting to buy homes. At first, homes for sale were scarce and there were lots of demand for homes. Due to the "supply and demand" principle, home prices began to rise. Lenders became even more free with their approving of loans because they felt that the risk was mitigated. Their thought was that if the mortgage holder defaulted, then the equity in the house due to the rising house prices would offset the costs of the foreclosure. People didn't care about having homes that were too expensive because they thought that if they got into trouble, they would just sell the home for a profit.

Of course, as home prices rose, contractors and home builders had more incentives to build more houses. A wave of home building took place. This increased the supply of homes for sale leveled off the price of homes. Now, homes are not increasing in value. There are now more homes for sale than there are buyers...and the price of the house is falling.

The built-in risk mitigation method from the bank and the plan of the loanee are gone. The home-owner can't afford the rising payments and he can't sell the house. He is going to lose money. The bank forecloses on the home, but they can't sell it for what the loan value is. They are losing money instead of creating it. Investment firms and other banks have wised up to the misrepresented packages and don't want to buy mortgages from other banks.

Putting it all together

Remember that $100,000 in immediate profit that the bank received when they sold your mortgage to another bank/investment firm. Well, that $100,000 becomes part of the cash reserve. What happens when investment firms and banks STOP buying mortgages or are unable to sell mortgages? Well, if they can't resell the mortgage, then they quickly reach their federally mandated cash reserve. Since they have to keep so much money in reserve, and they can't sell their loans...they can't give out anymore loans. Remember banks make money by making loans. If they can't make loans, they can't make money. They can't pay their employees. They can't pay their utility bills. They can't return their customers money when the customer calls for it because they don't have any. Its tied up in "Joe's house."

The banks that have been sold are those that could no longer manage to keep enough cash reserves to meet their own obligations.

The problem will trickle down to us everyday folks soon. See, people looking for loans for business opportunities can't get loans right now. The inability for banks to make loans or sell loans is FREEZING the economy.

See most business make by "leveraging" other people's money. This just a fancy term that means, a business will borrow a set of money to produce a product that will sell for more than what they borrowed. For example, let's say that I have a product that will make me $1,000,000. However, to produce the product it costs $200,000. Well, I don't have $200,000. So I go get a loan and "leverage" other people's money to make my $800,000 (yeah, I have to pay back the loan).

This is how many big companies do business. They don't have the cash on hand to produce new products for us to buy. They get a business loan. Since banks can't make loans, businesses can't make products. A steady demand for the products with a limited supply will cause those products to raise prices. So, we will shortly see even more stuff becoming more expensive. The more expensive, the less people buy. The less people buy, the less profits for companies.

People's incomes will not be going up (people may actually be laid off as their companies can't afford to pay them). Higher prices, same wages or lower wages. If more and more companies can't pay their people, more mortgage loans will default. As more loans default, there will be less incentive for banks and investment firms to buy mortgages...and you can see the downward cycle...

Conclusion

So, the government's plan is to "grease" the wheels of the economy by buying the bad loans. This will give the banks and investment firms the cash reserves they need to be able loan money and keep our economies wheels moving.

I still don't agree with the solution, but at least it makes more sense to me now.

1 I don't like the term "greedy" because it is so hard to really define. I know it is one of the "seven deadly sins." I think it just is bantered about too much and is very subjective.

However, even smart, economic people seem to think that there is a crisis. So, even though I don't see it, I need to understand it because my children and I look like we will be paying for "the solution." Here is my very poor attempt to distill the complicated problem into a simple explanation that can be understood by "everyman."

How banks work

To understand the problem, we need to first understand how banks work. Banks make a profit by loaning money. The funny things is that they don't loan their own money, they loan our money. We deposit our money in a bank to keep it safe for us. The bank then turns around and gives it to someone else in order to make money for itself. Banks can legally extend considerably more credit than they have cash. Still, most of us have total trust in the bank's ability to protect our money and give it to us when we ask for it.

Think back to Jimmy Stewart in "It's a Wonderful Life." There is a scene where there is a "run on the bank." A "run on the bank" is a panic that occurs when a large number of customers of a bank withdraw their deposits because they fear the bank is about to fail. So, all of the people who have deposited their money with George Bailey are clamoring for their money back. George tries to explain that he doesn't have their money, that it is tied up in other people's homes. He says,

"No, but you... you... you're thinking of this place all wrong. As if I had the money back in a safe. The money's not here. Your money's in Joe's house...And in the Kennedy house, and Mrs. Macklin's house, and a hundred others. Why,you're lending them the money to build, and then, they're going to pay it back to you as best they can."George ends up using his own money to give his customers the cash they want and saves his bank.

The Bank's Cash Reserve

So, banks make money by making loans. The amount of money a bank can lend is set by the Federal Reserve. This money that the bank is not allowed to lend is called the reserve (the reserve requirement is currently 3 percent to 10 percent of a bank's total deposits). This reserve is used to pay-out when bank customers need to use their money.

How The Mortgage Loan Industry Works

So, this crisis has its roots in the "sub-prime" mortgage industry. Basically, it used to be that to get a loan from a bank to buy a house it took a 20% down payment, several years at the same job, a great credit score, etc... These are all hard things to get. Saving up 20% of the purchase price takes fiscal discipline over a sustained period of time. It showed banks that you were a responsible and disciplined individual who could be trusted.

As you can well imagine, these requirements were a barrier to home-ownership. It was hard to get in a position to be eligible for a loan. Home-ownership is one of the primary means of building wealth. The government thought it would be good to help people achieve home ownership so that people could build long-term wealth. They, therefore, set up some programs with lower hurdles to jump.

One can now get FHA loans, VA loans, and other loan programs that do not require the same standards of fiscal discipline. I actually have an FHA loan and was able to get a mortgage with a pitiful 3% down-payment. The banks are willing to give people without a proven track record of financial discipline a loan because these types of loans are insured by the Federal government. If I fail to pay my mortgage, then the bank knows that the Federal government will pay-off the loan. The bank will not lose its money so it loans the money to people that are more likely to default on the loan.

In an effort to loan even more money, banks created new type of loan known as "sub prime" loans. These are loans that are made to people that do not meet Fannie Mae or Freddie Mac guidelines. Reasons for this might include credit status of the borrower (they have declared bankruptcy in the past, are consistently late on credit card payments, etc...), income and job history, and income to mortgage payment ratio (FHA guideline don't allow for the mortgage payment to be more than 38% of your income). So, now banks are loaning money to people who are at a much higher risk of defaulting.

Reselling Loans

Now, this where the banks began to be "greedy"1. Most banks and mortgage brokers DO NOT HOLD the loans they make. Once the loan is made is to an individual, the bank will then sell loan to another bank or investment firm. So, say the bank gives you a loan for $250,000 for 30 years at 6.5%. Over the next 30 years you will pay a total of $568,000: $250,000 (principle) and $318,000 in interest (i.e., that is the bank's profit). Well, a bank doesn't want to wait 30 years to get thier profit. So, they will sell the loan to someone else for $350,000. The bank gets an immediate $100,000 in profit and the investment firm is happy with $218,000 in profit (after 30 years).

Of course, the bank doesn't just sell one mortgage to the investment firm. Instead, they will package 100 mortgages that they originated all together and sell those to the investment firm. The investment firm doesn't look at the risk associated with each individual loan the bank originated, but a the package at whole. Some unscrupulous banks and mortgage brokers (knowing they would resell loan and not be liable for the risk) gave loans to people they knew could not repay the loan. These unscrupulous lenders would then misrepresent the risk of the package to the investment firm by mixing the package with both low-risk and high-risk loans.

The Housing Bubble

Easy access to home loans led to lots of people wanting to buy homes. At first, homes for sale were scarce and there were lots of demand for homes. Due to the "supply and demand" principle, home prices began to rise. Lenders became even more free with their approving of loans because they felt that the risk was mitigated. Their thought was that if the mortgage holder defaulted, then the equity in the house due to the rising house prices would offset the costs of the foreclosure. People didn't care about having homes that were too expensive because they thought that if they got into trouble, they would just sell the home for a profit.

Of course, as home prices rose, contractors and home builders had more incentives to build more houses. A wave of home building took place. This increased the supply of homes for sale leveled off the price of homes. Now, homes are not increasing in value. There are now more homes for sale than there are buyers...and the price of the house is falling.

The built-in risk mitigation method from the bank and the plan of the loanee are gone. The home-owner can't afford the rising payments and he can't sell the house. He is going to lose money. The bank forecloses on the home, but they can't sell it for what the loan value is. They are losing money instead of creating it. Investment firms and other banks have wised up to the misrepresented packages and don't want to buy mortgages from other banks.

Putting it all together

Remember that $100,000 in immediate profit that the bank received when they sold your mortgage to another bank/investment firm. Well, that $100,000 becomes part of the cash reserve. What happens when investment firms and banks STOP buying mortgages or are unable to sell mortgages? Well, if they can't resell the mortgage, then they quickly reach their federally mandated cash reserve. Since they have to keep so much money in reserve, and they can't sell their loans...they can't give out anymore loans. Remember banks make money by making loans. If they can't make loans, they can't make money. They can't pay their employees. They can't pay their utility bills. They can't return their customers money when the customer calls for it because they don't have any. Its tied up in "Joe's house."

The banks that have been sold are those that could no longer manage to keep enough cash reserves to meet their own obligations.

The problem will trickle down to us everyday folks soon. See, people looking for loans for business opportunities can't get loans right now. The inability for banks to make loans or sell loans is FREEZING the economy.

See most business make by "leveraging" other people's money. This just a fancy term that means, a business will borrow a set of money to produce a product that will sell for more than what they borrowed. For example, let's say that I have a product that will make me $1,000,000. However, to produce the product it costs $200,000. Well, I don't have $200,000. So I go get a loan and "leverage" other people's money to make my $800,000 (yeah, I have to pay back the loan).

This is how many big companies do business. They don't have the cash on hand to produce new products for us to buy. They get a business loan. Since banks can't make loans, businesses can't make products. A steady demand for the products with a limited supply will cause those products to raise prices. So, we will shortly see even more stuff becoming more expensive. The more expensive, the less people buy. The less people buy, the less profits for companies.

People's incomes will not be going up (people may actually be laid off as their companies can't afford to pay them). Higher prices, same wages or lower wages. If more and more companies can't pay their people, more mortgage loans will default. As more loans default, there will be less incentive for banks and investment firms to buy mortgages...and you can see the downward cycle...

Conclusion

So, the government's plan is to "grease" the wheels of the economy by buying the bad loans. This will give the banks and investment firms the cash reserves they need to be able loan money and keep our economies wheels moving.

I still don't agree with the solution, but at least it makes more sense to me now.

1 I don't like the term "greedy" because it is so hard to really define. I know it is one of the "seven deadly sins." I think it just is bantered about too much and is very subjective.

Thursday, September 25, 2008

Discipline is a Dirty Word

Discipline.

Nobody likes discipline. In our postmodern world we have shunned the concept of disciplining. Discipline is about boundaries. The postmodernist, though, sees rules as antiquated ideas used by those in power to control. To the postmodernist, there is no absolute truth, so there can be no boundaries.

Therefore, we don't practice self-discipline, indulging ourselves in whatever we fancy. We don't discipline our children for fear of hurting their little self-esteems. We live for the present, not caring about future consequences, under some illusion that because there are no boundaries, there are no consequences. After all, how can you have a consequence for crossing that which does not exist?

Our current "crisis" in the mortgage and financial sector are a result of a lack of discipline. Not fearing a consequence of their actions, they made irresponsible decisions. Now, with looming "bail-out," Congress is poised to ensure that they don't feel the consequences of their actions. They won't learn a thing!

The Hebrews writer reminds us that, "No discipline seems pleasant at the time, but painful. Later on, however, it produces a harvest of righteousness and peace for those who have been trained by it." (Hebrews 12:11). Yes, it would be bad for everybody if these companies were allowed to fold. It might even bring on a Depression. BUT...that is just the disciplining process. The end result of that happening, though, is that people and corporations will learn to be responsible. They will learn to be self-disciplined.

We are at a crossroads of philosophy. Do we listen to Timon's "Hakuna Matata" philosophy have "no worries" about how our present day actions will affect the future? Or, do we realize that the best way to teach people that a stove is hot is to let them get burned?

Inspired by John Stossel's column, "What happened to Market Discipline."

Nobody likes discipline. In our postmodern world we have shunned the concept of disciplining. Discipline is about boundaries. The postmodernist, though, sees rules as antiquated ideas used by those in power to control. To the postmodernist, there is no absolute truth, so there can be no boundaries.

Therefore, we don't practice self-discipline, indulging ourselves in whatever we fancy. We don't discipline our children for fear of hurting their little self-esteems. We live for the present, not caring about future consequences, under some illusion that because there are no boundaries, there are no consequences. After all, how can you have a consequence for crossing that which does not exist?

Our current "crisis" in the mortgage and financial sector are a result of a lack of discipline. Not fearing a consequence of their actions, they made irresponsible decisions. Now, with looming "bail-out," Congress is poised to ensure that they don't feel the consequences of their actions. They won't learn a thing!

The Hebrews writer reminds us that, "No discipline seems pleasant at the time, but painful. Later on, however, it produces a harvest of righteousness and peace for those who have been trained by it." (Hebrews 12:11). Yes, it would be bad for everybody if these companies were allowed to fold. It might even bring on a Depression. BUT...that is just the disciplining process. The end result of that happening, though, is that people and corporations will learn to be responsible. They will learn to be self-disciplined.

We are at a crossroads of philosophy. Do we listen to Timon's "Hakuna Matata" philosophy have "no worries" about how our present day actions will affect the future? Or, do we realize that the best way to teach people that a stove is hot is to let them get burned?

Inspired by John Stossel's column, "What happened to Market Discipline."

Wednesday, September 24, 2008

Ron Paul explains the Economic Mess

Here is an editorial by Ron Paul on the bailout. While I personally like Ron Paul's philosophy an and views, I find that so many of of his other supporters are just whacko. Anyway, it looks like he has economic problem well analyzed. Here are some quotes:

Laws passed by Congress such as the Community Reinvestment Act required banks to make loans to previously underserved segments of their communities, thus forcing banks to lend to people who normally would be rejected as bad credit risks.

...

The government doesn't like this [the fact that the market correcting itself producers winners and losers], however, and undertakes measures to keep prices artificially inflated. This was why the Great Depression was as long and drawn out in this country as it was.

...

Using trillions of dollars of taxpayer money to purchase illusory short-term security, the government is actually ensuring even greater instability in the financial system in the long term.

...The solution to the problem is to end government meddling in the market. Government intervention leads to distortions in the market, and government reacts to each distortion by enacting new laws and regulations, which create their own distortions, and so on ad infinitum.

It is time this process is put to an end. But the government cannot just sit back idly and let the bust occur. It must actively roll back stifling laws and regulations...

Tuesday, September 23, 2008

Bailout Expanded

The Washington Times is reporting that the bank bailout is being expanded to include student loans, car loans, and credit card debt.

This makes me so ANGRY. The government wants to take my money and give it to rich people who already have shown they are irresponsible with money.

I don't begin to think I understand the "economic" problem. However, I do know that the "bailout" money is going to banks and investment firms who are run by people paid really, really large sums of money to be profitable.

I also know that the government has NO money of its own. The only way for the government to get money to do things is to take that money by force from individuals1.

Our government is already in debt for over 9.7 trillion dollars. So, the only way for the government to give money to these banks and investment firms is to either pay with cash (which they don't have) or take out even more debt (which will have to be paid back in the future: so tax increases for me and my children).

I think as a taxpayer I am getting taken advantage of. I guarantee you that if Student Loans and Credit Card debt is added to the bail out, I will still cut two monthly check to Sallie Mae, a monthly check to DirectLoan and a check to Discover. In exchange for increased taxes in the future, I GET NOTHING!

Meanwhile, some Suit who made poor business choices gets to wipe his company's slate clean and start making TONS of money again.

So, here is my solution. If the government wants to bail someone out. Let them bail me out. If they wiped out my student loan and credit card debt, that would free up about 12% of my monthly budget. If they also "bail-out" my mortgage, then 32% of my budget would no longer be pre-set. Wow!!! If sending me $600 helps stimulate the economy, what could I do to stimulate the economy if I had over 30% of my budget free to invest and buy consumer goods EACH MONTH!!! Of course, I don't need a bail out because I am making all my payments.

Who needs to bail out the companies, who don't pay taxes when you can bail out the individuals who do pay taxes?

If the government does bail out the companies, then I want them to seize the assets of the companies and sell them off to subsidize some of the "bail out". Why should the American people get the raw end of this deal? Obviously the people running the companies are inept, so why should they be rewarded?

1Corporations don't pay taxes. All taxes "paid" by a corporation are really only taxes that the company has collected from individuals and passed on to the government. Corporations pass the taxes they owe to individuals through higher prices paid on products or they may not pay their individual employees as much. They may also not pay as much of a dividend to the shareholders (individuals) Trust me, in the mind of a corporation, taxes are a business expense and are somehow passed on to the individual. The company's profits are not affected by the tax code.

This makes me so ANGRY. The government wants to take my money and give it to rich people who already have shown they are irresponsible with money.

I don't begin to think I understand the "economic" problem. However, I do know that the "bailout" money is going to banks and investment firms who are run by people paid really, really large sums of money to be profitable.

I also know that the government has NO money of its own. The only way for the government to get money to do things is to take that money by force from individuals1.

Our government is already in debt for over 9.7 trillion dollars. So, the only way for the government to give money to these banks and investment firms is to either pay with cash (which they don't have) or take out even more debt (which will have to be paid back in the future: so tax increases for me and my children).

I think as a taxpayer I am getting taken advantage of. I guarantee you that if Student Loans and Credit Card debt is added to the bail out, I will still cut two monthly check to Sallie Mae, a monthly check to DirectLoan and a check to Discover. In exchange for increased taxes in the future, I GET NOTHING!

Meanwhile, some Suit who made poor business choices gets to wipe his company's slate clean and start making TONS of money again.

So, here is my solution. If the government wants to bail someone out. Let them bail me out. If they wiped out my student loan and credit card debt, that would free up about 12% of my monthly budget. If they also "bail-out" my mortgage, then 32% of my budget would no longer be pre-set. Wow!!! If sending me $600 helps stimulate the economy, what could I do to stimulate the economy if I had over 30% of my budget free to invest and buy consumer goods EACH MONTH!!! Of course, I don't need a bail out because I am making all my payments.

Who needs to bail out the companies, who don't pay taxes when you can bail out the individuals who do pay taxes?

If the government does bail out the companies, then I want them to seize the assets of the companies and sell them off to subsidize some of the "bail out". Why should the American people get the raw end of this deal? Obviously the people running the companies are inept, so why should they be rewarded?

1Corporations don't pay taxes. All taxes "paid" by a corporation are really only taxes that the company has collected from individuals and passed on to the government. Corporations pass the taxes they owe to individuals through higher prices paid on products or they may not pay their individual employees as much. They may also not pay as much of a dividend to the shareholders (individuals) Trust me, in the mind of a corporation, taxes are a business expense and are somehow passed on to the individual. The company's profits are not affected by the tax code.

Monday, September 22, 2008

Who caused the "Mortgage Crisis?"

As banks fall all around us and our financial markets take a beating, the media is pointing the finger at "greedy" capitalists.

However, are they really to blame?

Neal Boortz makes a compelling case that it we aren't being told "The Rest of the Story."

In his editorial, Neal recounts that 20 years ago or so the "BIG NEWS STORY" was that minorities and the poor could not get home loans. The media would run story after story showing where RACISM had prevented a minority from getting a loan, excluding the facts that the person seeking the loan had no money saved, no consistent job history, and a large pile of consumer credit card debt.

Congress told lenders that if they didn't shape up and find a way to get mortgages to these people, then congress would start regulating the industry even more. SO...the mortgage companies did find a way to give loans to people who weren't necessarily qualified. They developed a product called the "sub-prime" mortgage.

So. Who caused the mortgage crisis? Was it the "greedy" companies or was it an overzealous government? Or, was it a combination of both?

However, are they really to blame?

Neal Boortz makes a compelling case that it we aren't being told "The Rest of the Story."

In his editorial, Neal recounts that 20 years ago or so the "BIG NEWS STORY" was that minorities and the poor could not get home loans. The media would run story after story showing where RACISM had prevented a minority from getting a loan, excluding the facts that the person seeking the loan had no money saved, no consistent job history, and a large pile of consumer credit card debt.

Congress told lenders that if they didn't shape up and find a way to get mortgages to these people, then congress would start regulating the industry even more. SO...the mortgage companies did find a way to give loans to people who weren't necessarily qualified. They developed a product called the "sub-prime" mortgage.

So. Who caused the mortgage crisis? Was it the "greedy" companies or was it an overzealous government? Or, was it a combination of both?

Saturday, September 20, 2008

Book Survey: I Timothy

Erin and I are attending the Sunday School class on 1 Timothy this quarter. When I am a teacher, I hate it when people come to class unprepared. People want to have discussions in class about the subject matter, but how can I, as a teacher, facilitate a discussion when I am the only person who has taken the time to study the subject? That's one of the reasons most of classes are more "lecture" style than "discussion." I've studied the subject. I've become the expert.

Anyway, the teacher of the 1 Timothy class is a discussion teacher, so I am studying 1 Timothy so that I can contribute in a positive manner. I am using the methods that I taught to do the study. So, when studying a book, the first thing to do is the Book Survey method. Here is my Book Survey study of 1 Timothy.

Anyway, the teacher of the 1 Timothy class is a discussion teacher, so I am studying 1 Timothy so that I can contribute in a positive manner. I am using the methods that I taught to do the study. So, when studying a book, the first thing to do is the Book Survey method. Here is my Book Survey study of 1 Timothy.

Thursday, September 18, 2008

Recent Scripture Slides

I've only created two new scripture slides recently.

Genesis 1:2

Genesis 1:2

Hebrews 2:10

Hebrews 2:10

Genesis 1:2

Genesis 1:2 Hebrews 2:10

Hebrews 2:10Thursday, August 14, 2008

Twittering

Last week during in-service, the administration (after going to some conferences) of Erin's school was really pushing incorporating new technology in the classroom. They suggested that teachers make blogs, join MySpace, etc...

What is funny here is that when I was consulting for the school two ago, the administration wanted access to all that kind of information blocked. Now, they want to use it.

I think it is a futile idea because as soon as adults move into a student community, the students migrate away. As soon as something becomes mainstream enough that teachers use it, the students find some other technology or place to socially network.

The key, then, is to be ahead of the main stream adults. I told Erin if she really wants to be ahead of the curve, then she needs to begin using Twitter, because that is the next "big" social-networking type application. I am going to play with the service and see how it can be used for business and maybe how Erin can use it for school.

She can be the cool teacher for using it. It hasn't made it main stream yet, so it'll be a year or two before the school Administration gets wind of it. Of course, I fully expect them to want to block it first.

What is funny here is that when I was consulting for the school two ago, the administration wanted access to all that kind of information blocked. Now, they want to use it.

I think it is a futile idea because as soon as adults move into a student community, the students migrate away. As soon as something becomes mainstream enough that teachers use it, the students find some other technology or place to socially network.

The key, then, is to be ahead of the main stream adults. I told Erin if she really wants to be ahead of the curve, then she needs to begin using Twitter, because that is the next "big" social-networking type application. I am going to play with the service and see how it can be used for business and maybe how Erin can use it for school.

She can be the cool teacher for using it. It hasn't made it main stream yet, so it'll be a year or two before the school Administration gets wind of it. Of course, I fully expect them to want to block it first.

Monday, August 11, 2008

Mihaela prays

Part of the bed time routine is prayer. Usually, though, the kids will not pray and I have to pray "with" them. That's fine. I am modeling the behavior I want them to exemplify later in life.

Tonight I prayed with Noah and then went to pray with Mihaela. I said, "Let's pray" and she said, "I want to pray." I replied, "Of course you can pray."

She said:

My little girl starts school tomorrow and she is growing up too fast.

Tonight I prayed with Noah and then went to pray with Mihaela. I said, "Let's pray" and she said, "I want to pray." I replied, "Of course you can pray."

She said:

Dear God, Thank you for today. Thank you for mommy, daddy, Noah, and Lannom. Please help me to do good at school tomorrow. I love you Jesus. AmenI cried a little.

My little girl starts school tomorrow and she is growing up too fast.

Sunday, August 10, 2008

Biography of Paul

Our church, like many others, has difficulty finding teachers for Sunday School classes. This is especially true during the Summer Quarter. So, what we do each Summer is decide on some kind of theme, then we find 13 teachers and assign them a specific topic in that theme. Those teachers teach the same class twice (once in one room and once in another room, usually the next week).

This Summer we are doing biographies and I was asked to teach on the Apostle Paul. Now this is a challenge because how do you cover his biography in a single 45 minute class? You can't.

I just taught it my second week. I did it first in early July and then today...about 4 weeks in between. So, it wasn't as "fresh" to me today. Also, I was sick yesterday. On Friday my throat started hurting. Yesterday I started experiencing congestion, sinus headache, and general acheiness. I actually contemplated calling somebody to teach my class. Anyway, even though I wasn't feeling all that well, I went and taught my class. I felt punchy. My brain was certainly not "firing on all pistons."

I thought I did a good job, but I thought my first one was better. Erin disagreed. She said she was probably the only person who knew I wasn't feeling well and she thought I did a much better job this time.

Anyway, here are the lesson, a hand-out, and the PowerPoint.

Teacher Notes

Hand-out (Time-line Apostle Paul)

PowerPoint

This Summer we are doing biographies and I was asked to teach on the Apostle Paul. Now this is a challenge because how do you cover his biography in a single 45 minute class? You can't.

I just taught it my second week. I did it first in early July and then today...about 4 weeks in between. So, it wasn't as "fresh" to me today. Also, I was sick yesterday. On Friday my throat started hurting. Yesterday I started experiencing congestion, sinus headache, and general acheiness. I actually contemplated calling somebody to teach my class. Anyway, even though I wasn't feeling all that well, I went and taught my class. I felt punchy. My brain was certainly not "firing on all pistons."

I thought I did a good job, but I thought my first one was better. Erin disagreed. She said she was probably the only person who knew I wasn't feeling well and she thought I did a much better job this time.

Anyway, here are the lesson, a hand-out, and the PowerPoint.

Teacher Notes

Hand-out (Time-line Apostle Paul)

PowerPoint

Friday, August 08, 2008

Scripture Slides: The Backlog Edition

The scripture slides that I have posted seem to get the most Internet traffic from search engines. Anyway, with the posting problems I was having, I haven't uploaded any of the scripture slides that I have been working. So, here they are for your enjoyment. Click on the slide to get the higher resolution, better quality picture.

At the first of the year, Don did a seven-part series entitled "A Word to the Wise" where he discussed practical life issues with guidance from the book of Proverbs. So, I did a bunch of Proverbs slides. The Proverbs about wives, husbands, and marriage were not created for the "Word to the Wise Series" but were created for the recent "The Two Shall Become One" series.

Proverbs 1:8

Proverbs 1:8

Proverbs 2:6

Proverbs 2:6

Proverbs 3:6

Proverbs 3:6

Proverbs 3:9-10

Proverbs 3:9-10

Proverbs 6:23

Proverbs 6:23

Proverbs 10:4

Proverbs 10:4

(I don't really like this one...I need to learn how to do masking or layering or something better)

Proverbs 11:13

Proverbs 11:13

Proverbs 11:15

Proverbs 14:17

Proverbs 14:17

Proverbs 15:5

Proverbs 15:5

Proverbs 18:22

Proverbs 18:22

Proverbs 19:14

Proverbs 19:14

Proverbs 20:20

Proverbs 20:20

Proverbs 21:13

Proverbs 21:13

Proverbs 22:1

Proverbs 22:1

Proverbs 27:15

Proverbs 27:15

(I made this one as a joke. I double-dog dare anyone to actually use this one.)

Proverbs 31:10

Proverbs 31:10

This is the most recent slide I made. Don spoke just this past Sunday on this verse.

Deuteronomy 6:4

Deuteronomy 6:4

I made the next several slides for a sermon Don did entitled the "Abundant Life."

Ephesians 2:6

Ephesians 2:6

Jeremiah 29:11

Jeremiah 29:11

John 10:10

John 10:10

John 15:11

John 15:11

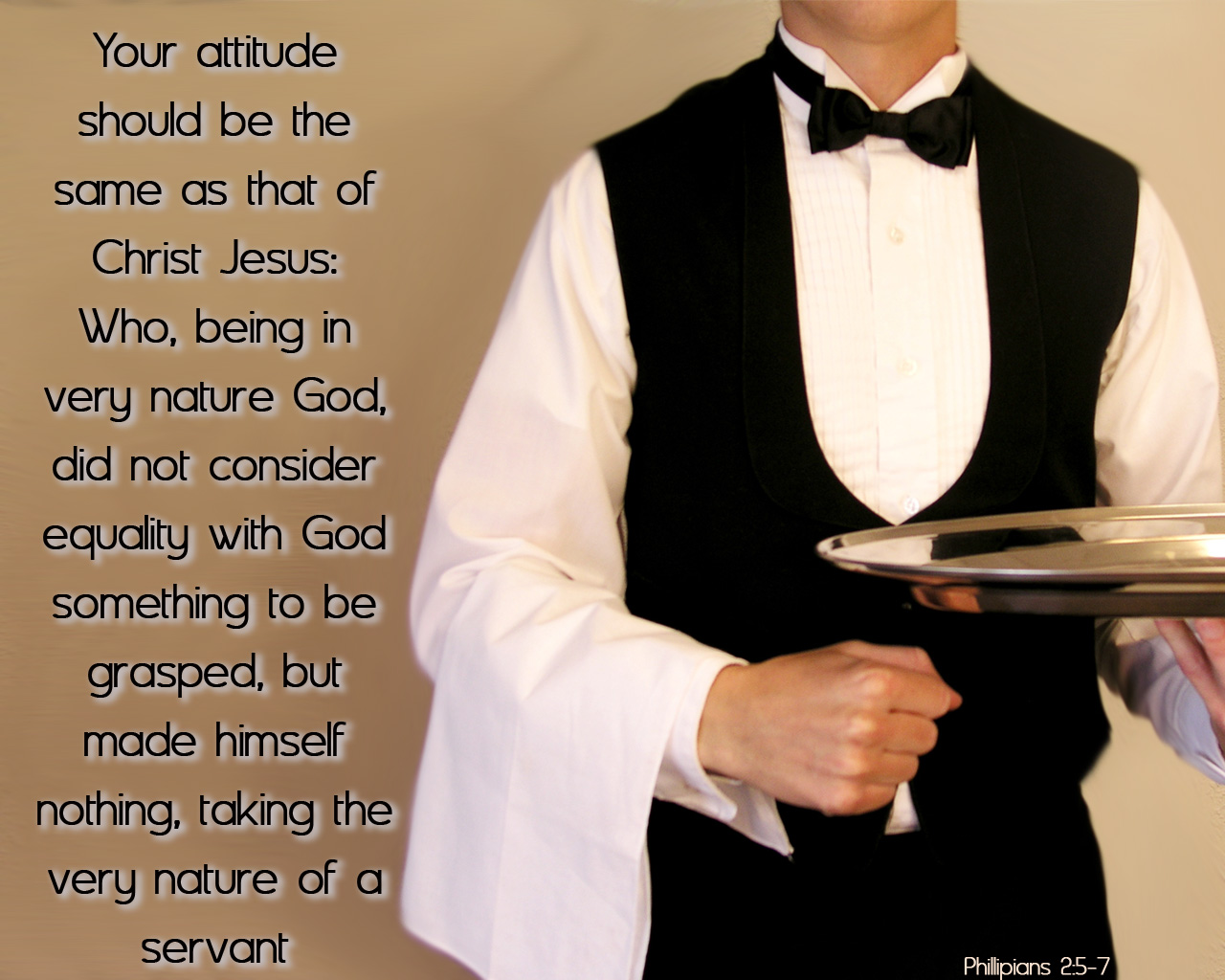

Philippians 2:5-7

Philippians 2:5-7

Philippians 4:4

Philippians 4:4

Psalm 16:11

Psalm 16:11

These last two (with some of the ones from Proverbs) were for the series on Marriage.

Song Of Solomon 4:10

Song Of Solomon 4:10

(I read through the book of Song of Solomon to find any passages that could be used. I had forgotten how explicit the book is. Even though it is very graphic, the author's tone exudes the purity of innocence in a marital relationship. Even so, I still became very uncomfortable reading the book; but not because of its frankness. Rather, I felt like I was intruder in the sacred intimacy.)

Ephesians 5:25

Ephesians 5:25

At the first of the year, Don did a seven-part series entitled "A Word to the Wise" where he discussed practical life issues with guidance from the book of Proverbs. So, I did a bunch of Proverbs slides. The Proverbs about wives, husbands, and marriage were not created for the "Word to the Wise Series" but were created for the recent "The Two Shall Become One" series.

Proverbs

Proverbs 1:8

Proverbs 1:8 Proverbs 2:6

Proverbs 2:6 Proverbs 3:6

Proverbs 3:6 Proverbs 3:9-10

Proverbs 3:9-10 Proverbs 6:23

Proverbs 6:23 Proverbs 10:4

Proverbs 10:4(I don't really like this one...I need to learn how to do masking or layering or something better)

Proverbs 11:13Proverbs 11:15

Proverbs 11:13Proverbs 11:15 Proverbs 14:17

Proverbs 14:17 Proverbs 15:5

Proverbs 15:5 Proverbs 18:22

Proverbs 18:22 Proverbs 19:14

Proverbs 19:14 Proverbs 20:20

Proverbs 20:20 Proverbs 21:13

Proverbs 21:13 Proverbs 22:1

Proverbs 22:1 Proverbs 27:15

Proverbs 27:15(I made this one as a joke. I double-dog dare anyone to actually use this one.)

Proverbs 31:10

Proverbs 31:10This is the most recent slide I made. Don spoke just this past Sunday on this verse.

Deuteronomy 6:4

Deuteronomy 6:4I made the next several slides for a sermon Don did entitled the "Abundant Life."

Ephesians 2:6

Ephesians 2:6 Jeremiah 29:11

Jeremiah 29:11 John 10:10

John 10:10 John 15:11

John 15:11 Philippians 2:5-7

Philippians 2:5-7 Philippians 4:4

Philippians 4:4 Psalm 16:11

Psalm 16:11These last two (with some of the ones from Proverbs) were for the series on Marriage.

Song Of Solomon 4:10

Song Of Solomon 4:10(I read through the book of Song of Solomon to find any passages that could be used. I had forgotten how explicit the book is. Even though it is very graphic, the author's tone exudes the purity of innocence in a marital relationship. Even so, I still became very uncomfortable reading the book; but not because of its frankness. Rather, I felt like I was intruder in the sacred intimacy.)

Ephesians 5:25

Ephesians 5:25Thursday, August 07, 2008

Unquestioned Authority or "I know more than you do"

Children are a wonderful blessing from God, full of surprises. I know (and expect) that we will have "issues" with our children as they grow older due to the fallen nature of man. Sometimes, though, I am caught off-guard by how seemingly early they exhibit certain behaviors.

For example, Lannom is now 16 months old. He LOVES to play with the screen. He KNOWS he is not supposed to play with it. Even at 16 months he will walk wrought iron fireplaceover and stand by it, then look to see if he is being observed before making his move. If we firmly say, "Lannom, No!" He will innocently look at us and blow us a kiss.

Last night I made dinner for the kids, popcorn chicken. When I gave it to Mihaela, she said, "MMMM....I love corn dogs." I replied, "Those aren't corn dogs, they are popcorn chicken." She then ARGUED with me that they were mini-corn dogs and clearly not popcorn chicken. She even went so far as to ask her Mom to set me straight.

I couldn't believe it. Four years old and she already knows more than I do. I thought I had a few more years of unquestioned authority on subject matters.

For example, Lannom is now 16 months old. He LOVES to play with the screen. He KNOWS he is not supposed to play with it. Even at 16 months he will walk wrought iron fireplaceover and stand by it, then look to see if he is being observed before making his move. If we firmly say, "Lannom, No!" He will innocently look at us and blow us a kiss.

Last night I made dinner for the kids, popcorn chicken. When I gave it to Mihaela, she said, "MMMM....I love corn dogs." I replied, "Those aren't corn dogs, they are popcorn chicken." She then ARGUED with me that they were mini-corn dogs and clearly not popcorn chicken. She even went so far as to ask her Mom to set me straight.

I couldn't believe it. Four years old and she already knows more than I do. I thought I had a few more years of unquestioned authority on subject matters.

Wednesday, August 06, 2008

Haven't Published: Moved Servers

Yeah....I know...its been quiet. I had some trouble posting using Labels with the FTP site I was using. So, I've moved servers. Let's see if this helps.

Also, I will be going back and posting the rest of Bible Study Methods class. Those will be back-dated.

Also, I will be going back and posting the rest of Bible Study Methods class. Those will be back-dated.

Monday, July 07, 2008

My Biography, My Testimony

For one of the Wednesday night classes this Summer the church has asked several members to share their testimony. I was asked to share my story.

I was very hesitant to do this because I didn't know that I had anything to really share. Anyway, I did agree to do it. To prepare for the class, I wrote an autobiography. I didn't know what I wanted to say, so the autobiography was just to make me think about stories and influences and what not. I just kept praying for the Holy Spirit to give me the words to speak.

When I went to the class, I still had no idea what exactly to speak on. When the Education Minister" introduced" me he mentioned that he had become intrigued with my background during my "How to study the Bible" class when I mentioned I had been a minister for a church planting in Wisconsin.

So, I knew then what stories to tell and thanked God for telling me what to say. I started by stating that I have never understood people who are "confused' about what God wants for their lives. God always seems to be moving me where He wants me, when He wants me to be there.

I then told different stories about how God had prepared me for ministry. I told the story of how we moved to Wisconsin. I told the story of how we left Wisconsin and how it was at just the right time. As I ended each story with the 20/20 hindsight of how God had worked, I re-iterated that I never understood people who are "confused' about what God wants for their lives.

Anyway, for prosperity, here is my autobiography. It is very boring. But, maybe in 20 0r 30 years my kids may want it.

I was very hesitant to do this because I didn't know that I had anything to really share. Anyway, I did agree to do it. To prepare for the class, I wrote an autobiography. I didn't know what I wanted to say, so the autobiography was just to make me think about stories and influences and what not. I just kept praying for the Holy Spirit to give me the words to speak.

When I went to the class, I still had no idea what exactly to speak on. When the Education Minister" introduced" me he mentioned that he had become intrigued with my background during my "How to study the Bible" class when I mentioned I had been a minister for a church planting in Wisconsin.

So, I knew then what stories to tell and thanked God for telling me what to say. I started by stating that I have never understood people who are "confused' about what God wants for their lives. God always seems to be moving me where He wants me, when He wants me to be there.

I then told different stories about how God had prepared me for ministry. I told the story of how we moved to Wisconsin. I told the story of how we left Wisconsin and how it was at just the right time. As I ended each story with the 20/20 hindsight of how God had worked, I re-iterated that I never understood people who are "confused' about what God wants for their lives.

Anyway, for prosperity, here is my autobiography. It is very boring. But, maybe in 20 0r 30 years my kids may want it.

Sunday, May 25, 2008

Unlocking God's Word: Week 12 - The Book Synthesis Method

A book synthesis involves tying a whole Book of the Bible together by summarizing and condensing what we learned using the previous methods.

Teacher Notes

PowerPoint (Free Microsoft PowerPoint 2007 Viewer)

The Book Synthesis Form

Teacher Notes

PowerPoint (Free Microsoft PowerPoint 2007 Viewer)

The Book Synthesis Form

Sunday, May 18, 2008

Unlocking God's Word: Week 11 - The Chapter Analysis Method

Chapter analysis involves gaining a thorough understanding of the material of a chapter of a book by looking carefully at each paragraph, sentence and word in an intensely detailed and systematic manner

Teacher Notes

PowerPoint (Free Microsoft PowerPoint 2007 Viewer)

The Chapter Analysis Method Form

The Chapter Analysis Observation Guide

Teacher Notes

PowerPoint (Free Microsoft PowerPoint 2007 Viewer)

The Chapter Analysis Method Form

The Chapter Analysis Observation Guide

Sunday, May 11, 2008

Unlocking God's Word: Week 10 - The Book Survey Method

A book survey involves gaining a sweeping overview of an entire book of the Bible. It is like standing on a bluff and looking over the terrain.

Teacher Notes

PowerPoint (Free Microsoft PowerPoint 2007 Viewer)

The Book Survey Method Form

Teacher Notes

PowerPoint (Free Microsoft PowerPoint 2007 Viewer)

The Book Survey Method Form

Sunday, May 04, 2008

Unlocking God's Word: Week 9 - The Background Method

This method allows you to gain a better understanding of the biblical message by researching the background related to the passage, person, event or topic being studied. This involves understanding the geography, historical events, culture, and political environment at the time a particular part of the Bible was written.

Teacher Notes

PowerPoint (Free Microsoft PowerPoint 2007 Viewer)

The Background Method Form

Teacher Notes

PowerPoint (Free Microsoft PowerPoint 2007 Viewer)

The Background Method Form

Wednesday, April 23, 2008

Unlocking God's Word: Week 8 - The Verse by Verse Analysis Method

In this method one chooses a very short passage of scripture and then scrutinizes that passage in detail from 5 different perspectives.

Teacher Notes

PowerPoint (Free Microsoft PowerPoint 2007 Viewer)

The Verse-by-Verse Analysis Method Form

Teacher Notes

PowerPoint (Free Microsoft PowerPoint 2007 Viewer)

The Verse-by-Verse Analysis Method Form

Sunday, April 13, 2008

Unlocking God's Word: Week 7 - The Character Quality Method

This method involves find out what the Bible says about a particular characteristic of a person, with heavy emphasis on personal application.

Teacher Notes

PowerPoint (Free Microsoft PowerPoint 2007 Viewer)

The Character Quality Method Form

Examples:

Teacher Notes

PowerPoint (Free Microsoft PowerPoint 2007 Viewer)

The Character Quality Method Form

Examples:

- Boldness (In-Class Example, form completed)

- Homework is not done yet. I'll update this post when I complete my homework. The assignment is to study the character trait of Humility.

Sunday, April 06, 2008

Unlocking God's Word: Week 6 - The Biographical Method

This method is one that allows a student to study the recorded life a person looking for ways to make positive character changes as a result of that study.

Teacher Notes

PowerPoint (Free Microsoft PowerPoint 2007 Viewer)

Handouts:

Examples:

Teacher Notes

PowerPoint (Free Microsoft PowerPoint 2007 Viewer)

Handouts:

- The Biographical Method Form

- List of Study Questions (assists in Step 5 of form)

- List of Character Traits (assists in Step 6 of form)

Examples:

- Stephen, the Martyr (In-Class Example, form completed)

- Homework will be updated when I finish my study. The homework is the study of Daniel.

Sunday, March 30, 2008

Unlocking God's Word: Week 5 - The Thematic Method

Our third method is a stripped down Topical Study. The student follows a theme through scripture.

Teacher Notes

PowerPoint (Free Microsoft PowerPoint 2007 Viewer)

The Thematic Method Form

Examples:

Teacher Notes

PowerPoint (Free Microsoft PowerPoint 2007 Viewer)

The Thematic Method Form

Examples:

- Jesus' Definition of a Disciple (In-Class Example, form completed)

- The Prayers of Jesus (Homework - this is my completed homework. Yours will different, and that is OK. I'm not posting this for you to see if you "got the right answers." This is here just in case your aren't feeling confident with the form yet, you can use this as another example. Obviously I want you to attempt to do it yourself first.)

Sunday, March 23, 2008

Unlocking God's Word: Week 4 - The Chapter Summary Method

This method is one that allows a student of the Bible to easily digest a chapter of the Bible. He starts by reading the chapter at least 5 times, aloud but quietly. Then, he uses the 10 "C's" to help summarize the central thoughts of the writer.

Teacher Notes

PowerPoint (Free Microsoft PowerPoint 2007 Viewer)

The Chapter Summary Method Form

Examples:

Teacher Notes

PowerPoint (Free Microsoft PowerPoint 2007 Viewer)

The Chapter Summary Method Form

Examples:

- Luke 15 (In-Class Example, form completed)

- I John 1 (Homework - this is my completed homework. Yours will different, and that is OK. I'm not posting this for you to see if you "got the right answers." This is here just in case your aren't feeling confident with the form yet, you can use this as another example. Obviously I want you to attempt to do it yourself first.)

Sunday, March 16, 2008

Unlocking God's Word: Week 3 - The Devotional Method

This is a our first of 10 methods that we will be looking at over the quarter. The Devotional Method is the easiest method to use because you just use one of the meditation techniques to chew on a passage of scripture until the Holy Spirit shows you a way to apply that to your life.

Teacher Notes

PowerPoint (Free Microsoft PowerPoint 2007 Viewer)

Handouts:

Examples:

Teacher Notes

PowerPoint (Free Microsoft PowerPoint 2007 Viewer)

Handouts:

Examples:

- Luke 12:22-26 (In-class example, form completed)

- I John 4 (Homework - this is my completed homework. Yours will different, and that is OK. I'm not posting this for you to see if you "got the right answers." This is here just in case your aren't feeling confident with the form yet, you can use this as another example. Obviously I want you to attempt to do it yourself first.)

Sunday, March 09, 2008

Unlocking God's Word: Week 2 - Principles, Preparations, and Problems

Week 2 of my "How to Study the Bible" class we cover some more theory.

Teacher Notes

PowerPoint

Handouts

Teacher Notes

PowerPoint

Handouts

Sunday, March 02, 2008

Unlocking God's Word: Week 1 - Using Your "Owner's Manual"

I am teaching a Sunday Morning Bible Class this quarter on "How to Study the Bible." I will be posting the materials here for others to use.

This first week is an introduction to the class and we discuss why we should study the Word of God and what Benefits we acquire from the study of God's Word.

Teacher Notes

PowerPoint

Handout

This first week is an introduction to the class and we discuss why we should study the Word of God and what Benefits we acquire from the study of God's Word.

Teacher Notes

PowerPoint

Handout

Saturday, March 01, 2008

The Socialist Republik of Kalifornia bans Home Schooling

A judge from the 2nd Appellate Court in Los Angeles has ORDERED that two children being home schooled must "be enrolled in a public school or "legally qualified" private school, and must attend."

While I don't know the specifics of the case (and have seen cases in the past where it was my opinion that parents were saying they were home schooling their children, and then not doing anything) what is most scary to me is the text in the judge's ruling where he denies that a parents right to religious freedom extends to the education of their children (emphasis added):

As California goes, so goes the rest of the US. So, in 10 to 15 years, as this philosophy works its way across the US we will find that our children must be surrendered to the control of the government. Parents who resist will face losing their children and/or criminal prosecution.

This is a common tactic of totaliatarian governments. Hitler banned home schooling in 1938 because he wanted the state, and no one else, to control the minds of the nation's youth. That law, by the way, has never repealed.

This is a byproduct of the Liberal-Socialism which is “progressively” gaining near absolute power over our lives in this country. They have taken over our schools in an attempt to indoctrinate our children in secular atheism, liberalism, militant environmentalism and sexual expression (both the acceptance of homosexualism and the advancement of sexual promiscuity in heterosexual relationships). They have been voted into power at the legislative level and clearly have grasped the reigns of the courts.

By controlling the minds, attitudes, and values of the children, they will stamp out the ideas of individuality and achievement. It may take 20 or 30 more years for them to see the fruition of what they are cultivating, but these children will grow up and vote. And then we will have "democratically" elected socialist. While we may never be ruled by a dictator, we will be ruled by 535 dictators to whom we willingly gave power. Whether it is one or 500, it is still a totalitarian government.

While I don't know the specifics of the case (and have seen cases in the past where it was my opinion that parents were saying they were home schooling their children, and then not doing anything) what is most scary to me is the text in the judge's ruling where he denies that a parents right to religious freedom extends to the education of their children (emphasis added):

"We agree … 'the educational program of the State of California was designed to promote the general welfare of all the people and was not designed to accommodate the personal ideas of any individual in the field of education.'"When it came to the parent's religious beliefs, the court responded:

In other words, according to the court in the state of California, the state has every legal right and authority to demand absolute control over the mind of children living in that state. Children are no longer legally under the control of their parents to help them grow in their belief systems, these poor children are the de facto wards of “The State.” The only thing the state wants from parents, is the financial support of the children.Their "sincerely held religious beliefs" are "not the quality of evidence that permits us to say that application of California's compulsory public school education law to them violates their First Amendment rights."

"Such sparse representations are too easily asserted by any parent who wishes to homeschool his or her child," the court concluded.

As California goes, so goes the rest of the US. So, in 10 to 15 years, as this philosophy works its way across the US we will find that our children must be surrendered to the control of the government. Parents who resist will face losing their children and/or criminal prosecution.

This is a common tactic of totaliatarian governments. Hitler banned home schooling in 1938 because he wanted the state, and no one else, to control the minds of the nation's youth. That law, by the way, has never repealed.

This is a byproduct of the Liberal-Socialism which is “progressively” gaining near absolute power over our lives in this country. They have taken over our schools in an attempt to indoctrinate our children in secular atheism, liberalism, militant environmentalism and sexual expression (both the acceptance of homosexualism and the advancement of sexual promiscuity in heterosexual relationships). They have been voted into power at the legislative level and clearly have grasped the reigns of the courts.

By controlling the minds, attitudes, and values of the children, they will stamp out the ideas of individuality and achievement. It may take 20 or 30 more years for them to see the fruition of what they are cultivating, but these children will grow up and vote. And then we will have "democratically" elected socialist. While we may never be ruled by a dictator, we will be ruled by 535 dictators to whom we willingly gave power. Whether it is one or 500, it is still a totalitarian government.

Friday, January 25, 2008

The Law of Unintended Consequences

Here is a guy who has the best explanation for how the law of unintended consequences operates, especially in how that deals with government regulation.

His last sentence explains why we have so many problems today:

His last sentence explains why we have so many problems today:

Does the law of unintended consequences mean that the government should never try to regulate complex systems? No, of course not, but it does mean that regulators should be humble (no trying to remake man and society) and the hurdle for regulation should be high.The issue we have is that our politicians today have NO HUMILITY at all. They think they know it all and treat the common with disdain. Secondly, since many of the current politicians were alive and active in the 1960's, they have a world-view that makes them think they already fundamentally changed society. (I personally believe society was already evolving. The action of the 60's may have sped up the process by 5-10 years, and the turmoil they caused was just the friction of making something move faster than it was intended to go). Because they think they did it once, they think they can do it again. Finally, there is no high hurdle for when to regulate. If any Sally, Jane, or Louise whines, then the politicians think they need fix a problem.

Thursday, January 24, 2008

Meaningless Economic Stimulus Package v 2.0

More information has come out about the package. I have to wonder, though, is it really a "stimulus" if checks won't be cut until June? We must really be in dire straits if we can wait 5 months for the fix (sarcasm).

It just goes to prove my earlier point that we probably don't really have a problem. Most of the reason people think we do is because of the extra hyperbole produced by a presidential campaign. Somebody is trying to "re-ignite" Clinton's 2002 win with "It's the Economy Stupid." Of course, to run on that platform, then the myrmidons must believe that the economy is bad. So, the candidates preach the economy is bad, the journalist endlessly repeat that the economy is bad, and the lemmings start believing the economy must be bad.

We have been raised to rely too much on experts and not enough on ourselves.

It just goes to prove my earlier point that we probably don't really have a problem. Most of the reason people think we do is because of the extra hyperbole produced by a presidential campaign. Somebody is trying to "re-ignite" Clinton's 2002 win with "It's the Economy Stupid." Of course, to run on that platform, then the myrmidons must believe that the economy is bad. So, the candidates preach the economy is bad, the journalist endlessly repeat that the economy is bad, and the lemmings start believing the economy must be bad.

We have been raised to rely too much on experts and not enough on ourselves.

Economic Stimulus is Meaningless

Many economist and experts believe that we are sitting at the precipice of recession, if we are not already in one. I'm not sure I believe them because my experience tells me that people are working and I still see lots of "hiring" and jobs available. However, for the sake of argument, I will concede that they are correct and assume that the economy is not doing well.

As in most cases these days, the government sees a problem and believes that they "have to do something." People read the papers, become worried, and demand solutions to the problem. They call their congressman and senators and ask, "How is the government going to protect me from this possible calamity?"

We've been hearing about a possible "economic stimulus package" that congress has been trying to deliver that will "fix" the problem. It appears that once again, the government thinks the best way to "fix" the problem, is to send everybody some money. The problem is, though, that this is not a solution.

Didn't we do this in 2001? It would seem to me that if sending everybody $300 would "fix" a recession, then we wouldn't need to do it again. So, that means that when this plan was tried 7 years ago, it didn't "fix" the problem, it only delayed the problem. It may temporarily "fix" a symptom, but it doesn't address the root causes of the economic problems. Why does congress think it will work this time?

The real issue I see is that the "common man" has chosen to burden himself with lots of personal debt and little savings. Many people have jobs, but are living paycheck to paycheck. Because the individual's financial situation is shaky, it causes people to feel that the economy is shaky. The truth is that $300 isn't going to "shore up" anyone's financial health. So, the most that this can do is give each family enough "extra" cash to frivolously spend while they think that the government has "helped" them.

The reality, though, will be that they are worse off because they will rush out to spend the $300, but instead buy something that is $350 or $500, thus increasing their debt load. So, they are still in the same financial situation (or worse), except they feel better because now they have a new flat screen TV, thanks to Uncle Sam.